August 2023 Market Update

Aimee Nairn

Consistent results and a solid reputation have earned Aimee the role of trusted advisor...

Consistent results and a solid reputation have earned Aimee the role of trusted advisor...

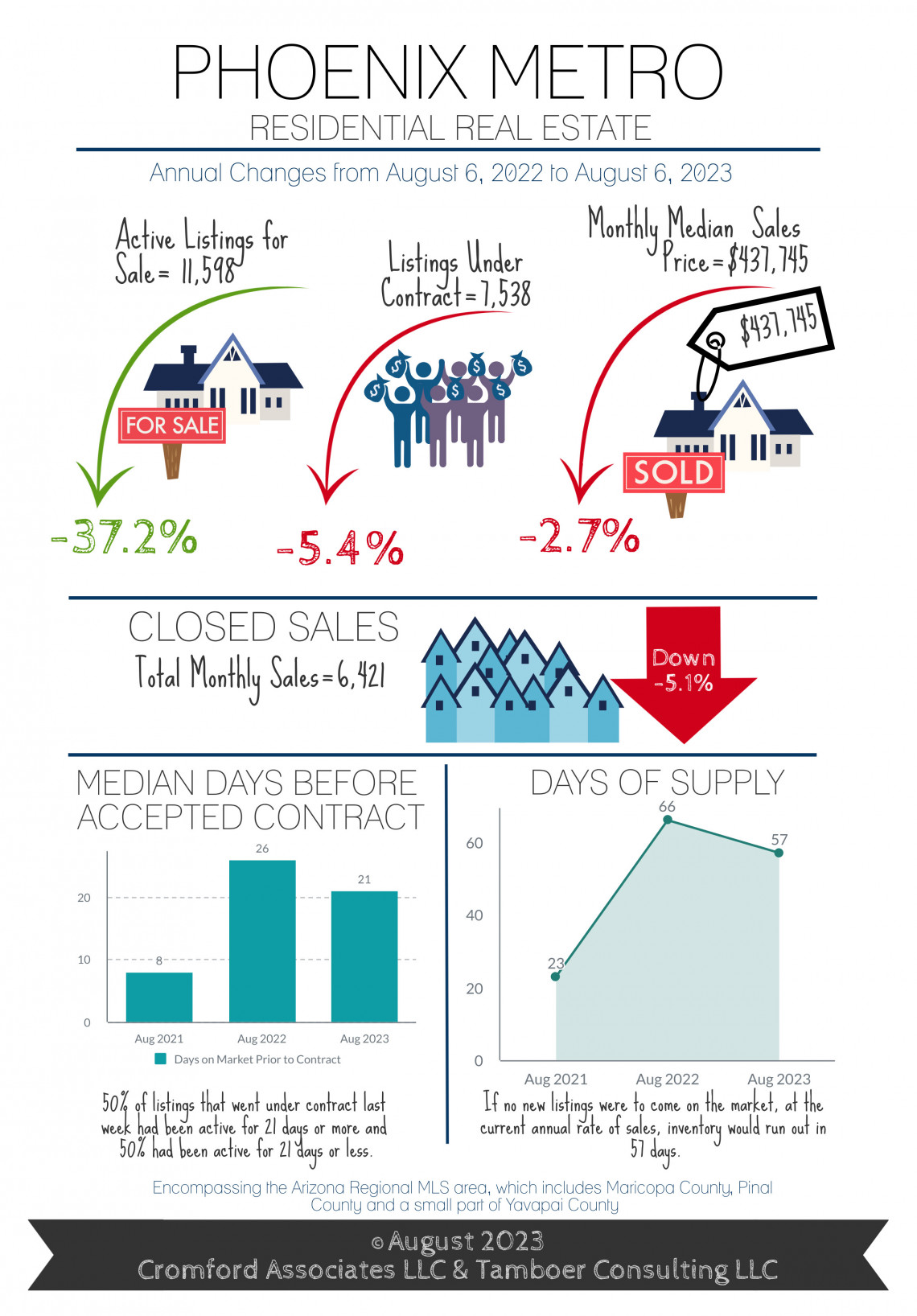

Active Supply Stabilizing, Still Down 39% From Last Year

Annual Appreciation Expected to Be Positive by September

For Buyers:

Not a lot of changes are happening in the housing market right now. It’s as if both buyers and sellers are in a holding pattern awaiting a sign before making a move. Conventional mortgage rates have held steady in the high 6% and low 7% range for nearly 3 months now with little signs of a decline yet. Rates have kept contract activity restricted since the 4th of July and overall demand 22% below normal for this time of year.

The continuous drop in supply we’ve been experiencing since October has slowed and flattened out over the past 6 weeks as well, but still 52% below normal for the past month and 37% below last year’s supply count. The ratio between supply and demand is keeping Greater Phoenix in a seller’s market, but it’s mild compared to the last 3 years. This indicates an upward pressure on price, but more subdued. Between September and December, the annual appreciation rate is expected to turn positive and may return to a pre-pandemic level similar to 2018 and 2019, which had annual appreciation rates between 5-8% on average.

This is good news for buyers for two reasons. First, the latter half of the year is typically the best time to be a buyer in Greater Phoenix as the highest months for closings are March through June. After June, buyer competition declines until the end of the year and gives buyers a little breathing room to tour homes and make decisions. Second, buyers understandably like to see their home’s value increase after they purchase, even if it's just a little bit.

There is also an expectation that the uncertainty surrounding mortgage rates may be lifted towards the end of the year or after the Federal Reserve concludes their meeting on September 20th. While mortgage rate predictions continue to be all over the board, and mostly wrong, if they do indeed decline over the next 3 months then expect both buyers and sellers to break their holding patterns and housing to move once again.

For Sellers:

While the Greater Phoenix market is experiencing its typical “summer slowdown”, marketing times prior to contract have held steady for the past 2 months at a reasonable 21 days. Also holding steady, 41% of closings involving seller-assisted closing costs, with the median cost to the seller at $8,000. Offsetting this statistic is a growing number of sales closing over asking price. June saw 21%, July 22%, and August is pushing 23% so far. In a normal seller’s market, this statistic doesn’t exceed 18% and typically peaks in June or July. The median amount over asking price for July closings was $6,000, and the majority of sales last month with both seller concessions and prices over list occurred on properties listed below $600,000.

New home construction is roughly a third of available inventory in the Arizona Regional MLS. While permit activity dropped significantly last year, this year it has bounced back, but not to the same level as 2022. Instead, new single family permits year-to-date are at a level Greater Phoenix hasn't seen since 2017. For existing homeowners, this means fewer new homes will be added to competing supply. Multi-family permits have outpaced single family and continue to hit new highs. The majority of these units are intended to be rentals, however, and will be adding little competition for existing owners of townhouses and condominiums.

The latest employment report for Arizona showed our state’s labor force continued to grow 2.5% year-over-year, faster than the U.S. growth rate of 1.8%. Non-farm employment grew by nearly 72,000 jobs and private sector earnings are up 2.4%. The unemployment rate is just 3.5%, well below the pre-pandemic measure of 4.9% and the lowest unemployment rate for Arizona since 2007. A diverse employment base and positive economic measures for Greater Phoenix continue to support price stability and a mild appreciation of home values through this period of restricted demand.

Commentary written by Tina Tamboer, Senior Housing Analyst with The Cromford Report

©2023 Cromford Associates LLC and Tamboer Consulting LLC

Thinking about selling?

Our custom reports include accurate and up to date market information.

Thinking about buying?

Everyone deserves to love where they live.